Life insurance doesn’t have to boring and just full of facts, figures, and numbers. Learning about life insurance can also be a fun exercise. Find out some of the most illuminating facts and figures about life insurance through our colorful and exciting infographic.

Go on! Take a peak below!

The illuminating Life Insurance infographic

Feel free to download this infographic and share it across your social media and websites.

So, you think insurance is all boring and serious? It doesn’t have to be. InsuranceLiya.com has comprised a list of the most mind bending wacky facts about insurance in this vibrant infographic. Enjoy!

Feel free to download this infographic and share it across your social media and websites.

Learn about The History of Insurance (Infographic)

So, you are interested in insurance and it’s antiquity? Let us take you down the rabbit hole, and through a journey that begins in 4000 BCE and ends today.

Check out the InsuranceLiya.com “History of Insurance Infographic”, and get a wholistic understanding about the lineage of insurance and insurance related products.

Let’s begin!

Feel free to download this infographic and share it across your social media and websites.

Learn how to check your vehicle’s PUC certificate online (In Simple Steps)

One should always have his vehicle’s Pollution Under Control (PUC) certificate handy. The PUC certificate is a mandatory document that can be demanded by the traffic police at any time, and not having it on hand can lead to fines and penalties.

A PUC certificate is directly disbursed by the place where the PUC test of your vehicle is undertaken. Take the PUC certificate and keep it within the vehicle at all times.

There are also times where you may want to check the validity of your PUC certificate. This article will shed some light on how you can check your vehicle’s PUC certification online.

Once you are on the VAHAN website, navigate to the “Online Services” section and click on “PUCC” from the dropdown.

Step 2: Click on “PUC Certificate” from the top bar

PUC certificate section

Step 3: Enter your details

PUC certificate page

Once on the PUC Certificate page, you will have to enter the following details:

Registration number

Chassis number

Security captcha

Press on the “PUC Details” button once all the above details are correctly entered.

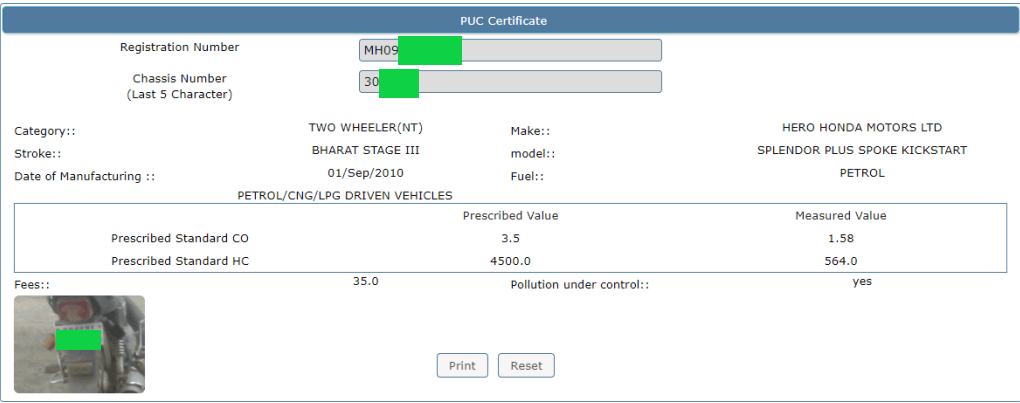

Step 4: Check your PUC certificate online

Example of PUC certificate

Here you can check the status and validity of your PUC certificate. Details mentioned within will be:

Registration number

Category

Stroke

Fuel type

Make of vehicle

PUC figures

We hope this article provided you with conclusive information on how you can check the status of your car/bike’s PUC status online using the Parivahan tool offered by the Ministry of Road and Highways of India. Always be safe, and always be prepared before each ride!

Top 2 ways to check your bike insurance expiry date online

You like to zoom across the streets and feel the wind in your hair? That’s awesome! But always remember to wear a helmet and ride your bike safely. It’s important to follow the rules of the road while you’re riding. It is also equally important to have always ride with a valid bike insurance policy with you. Let’s check out the top 2 ways you can check your bike insurance expiry date online, and be on top when it comes to renewing your bike insurance policy.

Check your expiry date via VAHAN

The VAHAN NR e-Services website is provided by The Ministry of Road Transport & Highways. VAHAN provides a host of beneficial services like transfer of ownership, change of address, issuance of vehicle fitness certificate, penalty payment, issuance of national permits, and more.

VAHAN also furnishes important vehicle centric information like:

Bike insurance expiry date

Bike registration date

Bike insurance status

Road fines levied on vehicle

Simply click on “Know your details” on top bar of the VAHAN website, and enter your registered mobile number in the next page, you will be redirected to a page where all vehicle centric details, including your bike’s insurance expiry date will be furnished.

VAHAN homepageVAHAN login page

There is another way you can check your bike insurance expiry date. It is through the IIB website. Let us see how you can do that below.

Check your expiry date via IIB

Step 1: Visit the IIB website

IIB homepage

Step 2: Click on V SEVA

Click on V seva

Step 3: Fill-in your details

V SEVA form

You will need to fill in your details like:

Name

Email ID

Mobile number

Address

Registration No

Step 4: Check your bike details

Post filling the form, you will be redirected to a portal where all your bike details (including insurance expiry date) will be furnished.

Apart from these two methods, certain insurance companies also provide an online feature on their respective websites where you can login and your policy details will be visible via the portal.

You can also check your insurance expiry date via your insurers website if they provide this feature.

All said and done, always be certain about the expiry date of your policy, and never ride with an expired insurance policy.

Crore

Vehicles registered with Parivahan (As of 2022)

Crore

Licenses issued by Parivahan

Lacs

Licenses issued in 2022 by Parivahan

Experience the power of Artificial Intelligence (A.I)

Chat with our super-intelligent A.I model and ask it anything about insurance and related products.

What is the difference between claim repudiation & claim rejection?

Have you ever come across the term “claim repudiation” and wondered what it meant? Is claim repudiation the same as claim rejection?

Let us briefly discuss the meaning of claim repudiation, and the difference between repudiation and rejection.

Meaning of claim repudiation

An insurance claim is said to be repudiated by the insurance company if the insurance policy does not provide any provision for disbursement of the claim for a particular condition or cause.

In simple terms, the cause that the claimant mentioned within his claim application is not a valid cause, and the insurance company does not consider it, thereby repudiating the claim.

Example of claim repudiation

Let us assume that Mr. Joseph has bought a motor insurance policy. A few years later, he meets with an accident while being under the influence of alcohol.

The motor insurance company will immediately repudiate his claim as it was clearly mentioned that no claims will be entertained if the policyholder meets with an accident under the influence of alcohol.

Thus the claim will not even be considered, and will be repudiated at once due to violation of policy terms.

Meaning of claim rejection

A claim rejection is when the cause of loss is valid, but the claim is rejected based on other factors. Common factors that lead to rejection are:

Falsifications by claimant

Improper documentation

Violation of company policy

Intentional mischief

Incomplete documentation

Delay in claim application

As mentioned in the article, there is a fine difference between claim rejection and claim repudiation. The general public should be aware of these finer differences, and always ensure that they go through the policy bond thoroughly with a fine-tooth comb at least once.

Also, please ask your insurance agent in case there are any doubts that are raised due to insurance lingo. It is their responsibility to clear all policy related doubts.

How to pay your LIC premium through debit or credit card? (Easy Guide)

Gone are they days where you would need to physically visit an LIC office and hand them over a check to make your premium payment.

LIC of India has successfully digitized itself, and now offer policyholders a host of high-tech services, which also include the ability for policyholders to make premium payments online through their debit/credit card.

Let’s find out how you can easily make your premium payment via debit or credit card.

There are 2 ways to make the premium payment; with login, and without login. We will elucidate both the methods below.

Make payment with login

Step 1: Visit the LIC online premium payment page

LIC online payment page

Visit the LIC online payment page by clicking here, and click on the “Pay Premium Through e-Services” button. Once you have clicked on that button, you will be redirected to the next page.

Step 2: Click on the “Registered User” button

Click on “Registered User”

You must now click on the “Registered User” button if you have your login credentials and password ready. Click on “New User” if you do not have an LIC e-Services account and want to create a new account.

Step 3: Enter your credentials and click on “Sign In”

LIC e-services login page

Once you are at this page, you need to enter your User ID/Email ID/Mobile along with your password and date of birth. Click on “Sign In” and login to your LIC e-Services account.

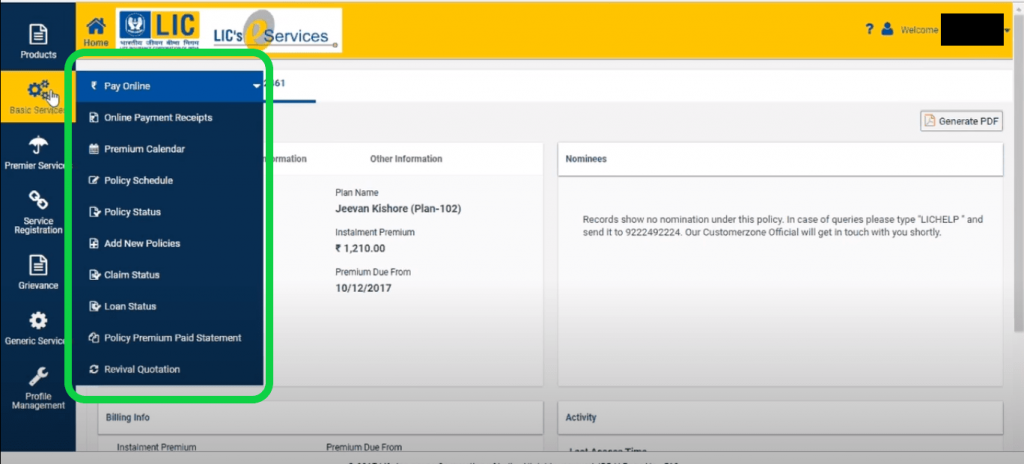

Step 4: Make the premium payment through Debit/Credit card

Once logged in, navigate to “Basic Services” and then click on “Pay Online”, then proceed to make the payment through your preferred debit or credit card.

Make payment without login

Step 1: Visit the LIC online premium payment page

If you do not have an LIC e-services account, you can also make your premium payment directly without logging-in. Click on “Pay Direct”

Step 2: Select the “Renewal Premium” option from the drop down

Once on this page, click on the “Renewal Premium” drop down menu and click on “Proceed”. You can also make an advance premium payment using this tool.

Step 3: Enter your policy details

This is where you enter your policy details, such as:

Policy number

Date of birth

Phone number

Premium amount

Email ID

Once entered, select “I Agree,” and click on “Submit”

Step 4: Make payment

Next, you will be redirected to the payment gateway page, where you can make your premium payment through your debit or credit card.

The current Chairman of LIC of India is Mr. Mangalam Ramasubramanian Kumar. Mr. M.R Kumar was appointed as The Chairman of LIC in 2019. He also previously held positions such a regional manager, and even Executive Director of LIC.

Mr. M.R Kumar was instrumental in The LIC IPO which hit the Indian Stock Market in 2022.

Mr. M.R Kumar currently holds positions in LIC, LIC Housing Finance, ACC, LIC Pension Fund, and LIC Cards Services Ltd.

Some of the key milestones of LIC of India

Let us now look at some of the most important key milestones that The LIC realized in recent memory.

In 2022, LIC of India entered the Indian Stock Market with the biggest IPO in India’s history, at Rs 21,000 crore.

As of 2022, LIC operates from within over 2000 branches Pan-India.

Over 2 crore new policies were sold by LIC in 2020 alone.

LIC of Indian is the largest asset management company in India, with assets under control worth over Rs 40 lac crores.

Experience the power of Artificial Intelligence (A.I)

Chat with our super-intelligent A.I model and ask it anything about insurance and related products.

How to get a duplicate LIC policy copy? (In 4 simple steps)

There are times when we might misplace or lose important insurance documents. It is important to stay calm and search for these documents with a clear head. However, if the document is still not found there are ways to attain a duplicate copy.

An original policy bond will be needed at many junctures, including when you want to claim the sum assured.

Let us talk about what you can do in case you misplace your original LIC policy bond, and how you can get a duplicate policy bond.

Steps to get a duplicate LIC policy copy

Step 1: Newspaper publication of advertisement

First, you will need to publish an advertisement in a well-circulated newspaper of your choice. Once you have published this advert, you will have to wait for a month and submit a cutting of the advert to your nearest LIC office.

Example of an LIC policy lost newspaper Ad.

Step 2: Make and submit an indemnity bond

Next, you will have to submit an indemnity bond to LIC. Ensure that you have a word with the designated LIC officer about the contents within the indemnity bond, the kind of stamp paper required, the number of witnesses required, etc. If possible, show a rough draft to the officer first, once he clears this draft, then you can proceed with making the actual indemnity bond.

An example of a 100 Rs stamp paper.

Step 3: Elucidate why and how the policy bond was lost

Once the indemnity bond is filled, you will be given a form (form 3756) that is required to be filled by the policyholder. The form will ask you for the following important details:

Name of original policyholder.

Why/how the original policy bond was lost?

Where was the policy bond lost?

Step 4: Fill-in the paperwork

Fill in all the details within form 3756 clearly and concisely, and ensure that there is no falsification within the form. Once the form is filled, you will be required to attach the following documents:

Insurance premium receipts

ID along with residential proof

Payment receipt (for issuance of duplicate bond)

Once all of these details and documents are furnished to LIC, they will verify the documents, do a background check, and then proceed with the issuance of a duplicate policy bond to the policyholder.

Experience the power of Artificial Intelligence (A.I)

Chat with our super-intelligent A.I model and ask it anything about insurance and related products.

No. Health insurance premiums do not increase every year. Premiums increase based on age slabs. For instance, an insurance company may have a fixed rate of premium for people aged 45-50, so a 45 year old policyholder will have to pay the same premium rate till he turns 50. The policyholder will only have to pay the increased premium rate after he turns 51 years of age.

Does health insurance premium increase every year?

Having a health insurance policy is critical in today’s day and age, where illnesses and diseases are rampant. Having a health cover will not reduce the chance of being diagnosed with a medical condition but it will at least provide a financial cushion in the event of hospitalization.

You may also have the question “Do health insurance premiums insurance every year?” The answer is no. Health insurance premiums do not increase every year, they increase periodically based on age slabs. Let us understand this with a simple example.

Let us assume that Mr. Rakesh (aged 24) bought a health cover from Reliance Health Insurance, paying a premium of Rs.10,000. Mr. Rakesh will continue paying Rs.10,000 till the age of 30. Then post the age of 30, his premium will increase to Rs.15,000. He will continue paying Rs.15,000 from the age of 31 to the age of 45. Then post 45 his premium will again increase. This is how a health insurance premium generally increases.

This is an example of a premium slab

Why does health insurance premium increase?

Now, let us find out why health insurance premiums increase.

Medical inflation has been increasing at 15% a year compared to general inflation which is increasing at 6-7% a year. The insurance companies need to account for this by charging higher insurance premium.

As talked about before, health insurance companies also increase the premium based on age slabs. As and when a person enters a particular age slab, his health insurance premium will increase accordingly (Kindly refer to Mr. Rakesh’s example above).

The premium will also increase if the policyholder purchases additional riders that increase coverage.

How can I counter the increase in premiums?

Let us now talk about some of the ways a policyholder can reduce his premium load in the face of constantly increasing premiums.

A policyholder can find a different policy with a different insurance company, and port his existing policy to a different policy. This is called as porting of a health insurance policy. One should ensure that the benefits and coverage of both policies are the same, only the price factor should be different. That way, you get the same benefits at a lower price.

A policyholder can also opt for a family floater plan. This is where the entire family is covered under a single health insurance policy.

Ask your insurance agent to give you the best possible deals. If you do not ask, you may miss out on any new deals, offers and benefits.

$ Billion

Gross premium collected by General Insurance Companies in India (As of 2022)

$ Billion

Gross premium collected by Life Insurance Companies in India (As of 2022)

% Insurance Penetration

Total life insurance penetration stands at a slender 3.2% (As of 2021)

Experience the power of Artificial Intelligence (A.I)

Chat with our super-intelligent A.I model and ask it anything about insurance and related products.